Fixed Income investments in FY22

Fixed Income investments in FY22

Fixed income investments in FY22 | Barbell Strategy | 5 debt funds

Equities are exciting. Fixed income is boring. Most investors should stay away from debt funds and stick to FD, NSC, PPF, RBI Floating rate bonds, etc. Debt funds ARE risky and for most investors that extra 1% - 1.5% is not worth the risk.

We have entered FY22 (2021-22) with interest rates low and expected to rise over the next 12-18 months1. Investors are looking at low returns on the safe short term debt instruments.

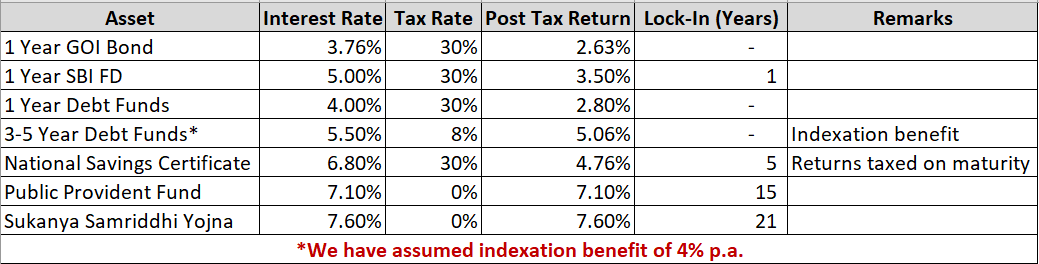

1 Year G-Sec: 3.76%

1 Year SBI FD: 5%

The mutual fund schemes which can be considered the safest for short duration investments are no different. The overnight, liquid, money market and ultrashort duration funds have an average YTM of 3.35% to 3.97%, not accounting for the expense ratio. These category of funds have maturities of less than 6 months.

Investors should consider taxation before deciding on fixed income instruments. Debt funds held for more than 3 years come under long term capital gains tax and you pay 20% tax AFTER indexation benefits. So, if your tax slab is 30% or higher, then you are better off investing in debt funds over FDs.

Debt funds held for less than 3 years are taxed as per your income tax slab rate and it is no different than fixed deposits.

Barbell Strategy

The debt fund managers seem to be following a re-investment strategy or a barbell strategy. This strategy is usually adopted when interest rates are expected to rise. Under this strategy, the fund managers invest in very short duration papers and very long duration papers. The amount invested in very short duration papers mature in a few months are then re-invested at higher rates as the interest rates increase. The long duration bonds provide with steady cash flows and at the same time provide some security in case interest rates fall.

Where to invest for < 2 years for highest returns with lowest risk?

Simply put your money in a short duration FD or liquid fund. 0.5% difference in returns would hardly make a difference for retail investors. However, if you like making the best out of a situation, then consider this:

Open a savings account with IDFC First Bank. The interest rate on savings account deposits upto Rs 1 Crore is 6% p.a.2 Now as per DICGC rules, deposits in a particular bank are insured upto Rs 5 Lakhs. So, the safest investment with highest returns for investors looking to invest for < 1 year is the savings bank account of IDBI First Bank. This option is highly liquid and you can withdraw your funds whenever required. Infact, it is more liquid than liquid funds! Now, IDFC First Bank can at any time slash interest rates as they recently had from 7% to 6%3

Where to invest for 2-5 years?

This is the trickiest time frame in current times for fixed income investors. The short duration maturity debt funds mentioned above are hardly giving 4% p.a. Instruments like NSC, PPF and Sukanya Samriddhi have long lock-ins ranging from 5 years to 15 years! The fixed deposit rate on as SBI FD for 3 to 5 years is 5.3%. For this investment horizon, we believe that investors should consider debt funds as they are tax efficient if held for 3+ years.

ICICI Prudential Credit Risk Fund

Credit risk funds have to invest 65% of their portfolio in AA or lower rated securities. So they aren’t the safest. However, their papers mature in 1-3 years and thus they aren’t very sensitive to interest rate risks. Credit risk funds are best left to those who understand credit risk and can actively track a fund’s portfolio on a monthly basis. For others, you can avoid this risk to earn an extra 1.5% to 2% p.a.

The ICICI Pru Credit Risk Fund has a YTM of 7.82% and an expense ratio of 0.9% so if all goes well, then an investor can expect to make ~ 6.9% p.a. pre tax over the next 15-18 months in this fund.

ABSL Corporate Bond Fund

This fund has 96% of its portfolio in SOV/AAA/A1+ rated papers. The average maturity of its papers is 2.87 years. The current YTM is 5.37% and expense ratio is 0.28%.

Kotak Corporate Bond Fund

This fund has 100% of its portfolio in SOV/AAA/A1+ rated papers. The average maturity is 2.1 years. The current YTM is 5.2% and expense ratio is 0.27%.

Nippon India Short Term Fund

This fund has 86% of its portfolio in SOV/AAA/A1+ rated papers. The average maturity is 2.51 years. The current YTM is 5.58% and expense ratio is 0.34%.

HDFC Short Term Fund

This fund has 81% of its portfolio in SOV/AAA/A1+ rated papers. The average maturity is 2.8 years. The current YTM is 5.51% and expense ratio is 0.34%.

Where to invest for 5-10 years or more?

If you are looking to add fixed income instruments to your long term portfolio (Read 8-10 years or more), then we highly recommend instruments like Sukanya Samriddhi Yojna, Public Providend Fund and the National Savings Certificate. The interest rates on these instruments keeps getting revised regularly4, and if interest rates rise, then these instruments will also fetch you higher returns.

Sukanya Samriddhi Yojna: 7.6% (Tax free)

Public Provident Fund: 7.1% (Tax free)

RBI Floating Rate Bond: 7.15% (Simple interest)

Kisan Vikas Patra: 6.9%

National Savings Certificate: 6.8%

10 Year GOI Bond: 6.1%

The best time to invest in G-Sec debt funds and long duration debt funds is when the interest rates are expected to come down. For now, avoid long duration debt funds.

Why tax shouldn’t be ignored

For > 3 years, the indexation benefits reduce your tax outflow on the returns from debt funds. Indexation benefits in simple terms, increase the purchase price of your debt funds in-line with inflation (the Government every year publishes the index chart)5.

https://economictimes.indiatimes.com/wealth/invest/why-fixed-depositors-investors-can-expect-higher-interest-rates-ahead-and-what-they-should-do-now/articleshow/81223083.cms

https://www.idfcfirstbank.com/content/dam/idfcfirstbank/interest-rate/Interest-Rate-Retail.pdf (Read page 4)

https://www.livemint.com/industry/banking/idfc-first-bank-cuts-savings-account-interest-rate-to-6-from-1st-february-11612150217962.html

https://economictimes.indiatimes.com/wealth/personal-finance-news/ppf-to-fetch-6-4-nsc-5-9-as-govt-cuts-interest-rates-on-post-office-schemes/articleshow/81719887.cms

https://economictimes.indiatimes.com/wealth/tax/cost-inflation-index-for-fy-2020-21-used-for-ltcg-calculation-notified-by-finance-ministry/articleshow/76355897.cms?from=mdr